There is considerable debate on whether or not President Trump’s tariffs are creating inflation. Many economists argue that tariffs are inflationary because they directly raise the cost of imported goods and may lead to higher prices for domestic alternatives. This perspective was echoed by former Federal Reserve Chair Janet Yellen, who stated in 2022, “Tariffs tend to boost domestic prices and make goods more expensive.” This article will examine the data to determine whether tariffs are causing inflation.

When a government imposes tariffs on imports, the immediate effect can be raising the price of those imported goods. And, if domestic producers also increase their own prices, this can create upward pressure on the overall price level—an effect referred to as inflation.

However, some analysts believe the inflationary impact of tariffs depends on context. For instance, if tariffs are targeted at goods with plentiful domestic alternatives, or if the affected imports are a minor component of household spending, the inflationary effect might be muted. The Congressional Research Service notes: “The overall effect on inflation depends on the share of products subject to tariffs and the ability of consumers to substitute away from higher-priced imports.”

While there is agreement that tariffs tend to increase the prices of affected goods, the extent to which they contribute to overall inflation depends on the structure of the economy and the scope of the tariffs. Most empirical evidence suggests tariffs do put upward pressure on prices, but the scale and significance can vary.

After President Trump announced new and expanded tariffs on a wide range of Chinese imports in 2025—covering sectors like electric vehicles, batteries, and advanced technology—economists expressed their opinions on the likely impact on inflation. Here’s an overview of professional opinions from several economists and economic organizations:

1. Goldman Sachs

Goldman Sachs economists argued that “The new tariffs are likely to have a small direct impact on inflation, since the targeted products account for a minor share of consumer spending. However, if tariffs are broadened or trigger retaliation, the impact could be more significant, especially if supply chains are disrupted.” However, they noted that “broader or retaliatory tariffs could have a more meaningful effect if they lead to supply chain disruptions or higher costs for intermediate goods.”

2. Lawrence Summers (Former U.S. Treasury Secretary and Harvard Professor)

Lawrence Summers criticized the 2025 tariffs, stating, “Tariffs are taxes that get passed on to consumers. The more tariffs, the more upward pressure on prices,” and that the new measures “risk modest but noticeable increases in prices for consumers, especially on goods made with Chinese components.”

3. Paul Krugman (Nobel Laureate, New York Times Columnist)

Krugman wrote that while the immediate, direct impact of the 2025 tariffs on inflation “will likely be limited and largely sector-specific,” there’s a risk that trade wars escalate: “Retaliation and further trade barriers could eventually seep into broader price increases.”

4. Moody’s Analytics (Mark Zandi, Chief Economist)

Mark Zandi of Moody’s Analytics stated the 2025 tariffs “will have a marginal, temporary effect on inflation,” estimating an increase of “less than 0.1 percentage point” on the Consumer Price Index in the following year. He cautioned, however, that “if the trade conflict escalates, the inflation impact could be more significant.”

5. Peterson Institute for International Economics

A policy brief from PIIE pointed out, “Past experience shows that tariffs are paid by U.S. importers and often passed on to consumers, though the 2025 set of tariffs mainly target industries where substitution is possible, potentially blunting the inflation impact.”

Summary Table

| Economist/Organization | Opinion on Inflation Effect | Source Link |

| Goldman Sachs | Small direct impact, higher risk if escalation occurs | GS Research |

| Lawrence Summers | Modest but noticeable upward pressure on prices | Financial Times |

| Paul Krugman | Limited sectoral effect, bigger risk if trade war escalates | NYT |

| Mark Zandi (Moody’s) | Marginal, temporary rise; more if conflict escalates | Moody’s Analytics |

| Peterson Institute (PIIE) | Tariffs paid by importers, inflation muted by substitutions | PIIE |

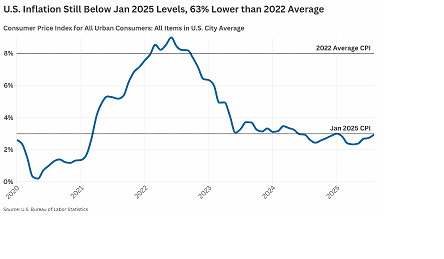

A September 25, 2025 report titled , “Tariffs Are Not Causing Inflation: Breaking Down August 2025 CPI” by Andrew Rechenberg of the Coalition for Prosperous America argues “Inflation today is moderate, running far below the post-COVID peak and even below January 2025 levels, before any new tariffs were enacted. Furthermore, the main drivers of August 2025 inflation are housing shortages, energy demand, and food supply shocks — not tariffs.”

The report breaks down the August Consumer Price Index showing that the following drivers for inflation were:

- Shelter: +0.4% m/m

- Airline Fares: +5.9% m/m.

- Beef: +2.7% m/m retail; +8% wholesale PPI.

- Coffee: +6.9% m/m.

- Electricity: +0.3% m/m

- Eggs: flat m/m, but +10.9% Year over Year

Surprising to economists was the fact that many imported goods were not the drivers of inflation as shown below:

- Autos: New vehicles rose +0.3% m/m and used vehicles +1.0% m/m

- Steel & Aluminum: +0.4% m/m

- Electronics: flat to +0.1% m/m

- Pasta, Olive Oil, and Spices: 0.0–0.2% m/m

Andrew concludes: “If tariffs caused “economic disaster,” inflation wouldn’t be at 2.9% — it would look like 2022 all over again. Inflation data does not support these dire warnings. CPI rose just 0.2% in August, while PPI actually declined. As shown in Figure 1, Inflation today is running 63% below the 2022 average and even just below January 2025 inflation levels, hardly the sign of an “economic disaster.”

In reality, an examination of the Consumer Price Index (CPI) from March 2025 to July 2025 shows that the main drivers of price increases (inflation) are similar to the August report examined by CPA.

1. Energy Prices

- Import-related: Increases in global oil and gas prices due to geopolitical tensions or supply constraints (e.g., OPEC+ production cuts, Middle East instability) drove up domestic fuel and electricity prices.

- Domestic: Infrastructure failures or domestic supply chain issues (e.g., refinery outages, grid failures) also boosted local energy prices.

2. Food Prices

- Import-related: Rising prices of imported foodstuffs (such as coffee, cocoa, grains, or meat) due to poor harvests, supply chain disruptions, or currency depreciation.

- Domestic: Domestic droughts, floods, or other adverse weather events affected local crop yields, and labor shortages increased local production costs.

3. Wages and Labor Costs

- Domestic: Wage increases from tight labor markets or new government policies (minimum wage hikes) led to higher costs for services and goods, which was passed on to consumers.

4. Rents and Housing Costs

- Domestic: Continued demand for housing, supply shortages, and higher mortgage interest rates pushed up rents and property costs.

As we can determine from data for the CPI from March to July 2025, the main drivers for inflation are related to domestic policies, not tariffs. Each of these drivers could be explored in separate articles, but that would be out of my area of focus and expertise.

Thus, I continue to support President Trump’s tariffs that will balance our trade deficit and help rebuild American manufacturing. I still believe that fluctuating tariffs on Chinese imports that are only temporary and at lower levels won’t have the lasting effect needed to rebuild America’s industrial base. Tariffs on Chinese imports need to be made permanent at a high level (100-125%) to influence CEOs of American companies to decide to reshore manufacturing to America, expand existing plants, and/or build plants in new locations. This action is truly the only way to Make America Great Again.