On October 13, 2016, the “Southern California Manufacturing Summit” was held at the Wedgewood Center in Aliso Viejo. The summit was hosted by the Coalition for a Prosperous America (CPA), with SDG&E/Sempra Utilities as the major sponsor, along with a long list of non-profit organizations, regional businesses and associations as sponsors and partners. The purpose of the summit was to learn and discuss how we can use Southern California’s advantages to re-grow manufacturing and create good paying jobs through smarter policies on trade, taxes, and the economy.

CPA is a unique alliance of manufacturing, agriculture, and labor working for smart trade policies and represents over three million households through our member associations and companies.

Since nearly all of our sponsors provide services that benefit manufacturers, we modified our format from previous summits to provide opportunities for our sponsors to tell about their services to promote networking among attendees.

Our first speaker was Greg Autry, Adjunct Professor of Entrepreneurship, Marshall School of Business, University of Southern California, who discussed “National Security Concerns with the Current U.S. Trade Regime.” Among the highlights of his presentation was his statement, “There are national security concerns with trade agreements. An economy that builds only F-35s is unsustainable – productive capacity is what wins real wars. Sophisticated systems require complex supply chains of supporting industries. They require experienced production engineers, machinists, and more.”

He recently prepared a report analyzing the competition and found that we are now outsourcing most of our space-related technology. He said, “NASA awards contracts for launch vehicles to Boeing and Space X, but chose to buy Russian lower stage engines. We have to choose if we are going to have a supply chain for the space industry. We cannot rely on China to produce what we need for our military and defense systems.

He added, “The International Space station was funded by the U. S. to the tune of $100 Billion of the $120 Billion that it cost. We should not be relying on Russia’s Mr. Putin to launch our satellites and space vehicles and provide us a seat to get to the international space station.”

Autry stated, “If you own stock in Alibaba, you actually own stock in a holding company in the set up in an offshore tax haven of the Cayman Islands, and the real owner behind Alibaba is the Chinese government. In contrast, he said, “It was the wealth he created at Amazon that enabled founder Jeff Bezos to now lead Blue Origin, which was selected by the United Launch Alliance to finish development of a new engine to replace the Russian made RD-180 rocket engine used by ULA’s Atlas 5 rocket.”

He pointed out that the Germans had the best technology in WWII, but didn’t win because we out produced them. Productive capacity is what wins wars. We wouldn’t be able to do the same for a future war as China has become the shop floor for too many American manufacturers. Take the U.S. F-22 airplane vs. the Chinese J20 airplane. We have 187 F-22s, and we stopped producing them because they were too expensive. China has several hundred J-20s, and they are still producing them.

He warned, “China has been an aggressive nation for thousands of years – it’s how the country grew from a small nation state. China has expanded their claim to territorial waters to include territory claimed by all of its immediate neighbors — Taiwan, South Korea, Vietnam, Japan, the Philippines, Japan and even New Zealand and Australia. China’s threat to these countries could eliminate getting supplies from Vietnam, Taiwan, and Korea, where companies are located that are now part of our supply chain for the military and space industry. We are going to lose our supply chain for the military and defense industry because the people in the State and Commerce Departments don’t talk to the Defense Department.”

After his presentation, July Lawton, President of The Lawton Group/TLC Staffing, explained that her company provides temporary to permanent staffing solutions for engineering, manufacturing, information technology, as well as the more traditional human resources, accounting, administrative, marketing, and healthcare positions.

Nicholas Testa, Jr., CFPIM, CSCP, CIRM, is founder and CEO of Acuity Consulting, Inc. a firm specializing in supply chain and operations management and systems consulting and training. He is president-elect of the APICS Orange County and described the types of supply chain education and training that APICS provides to its manufacturing industry members.

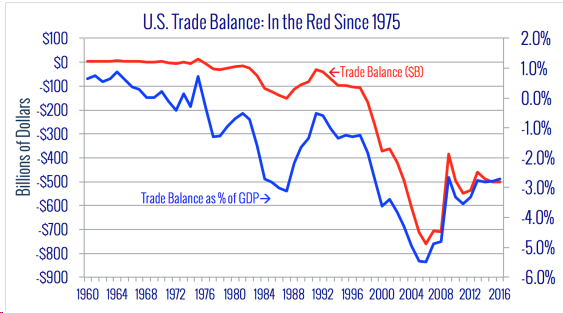

Economist Ian Fletcher, author of Free Trade Doesn’t Work” was the next speaker. A few highlights of his presentation were: “Free trade is trade without restrictions. Economic rivalry is taking place every day. There is rivalry for wealth and power. We live in America, and it does matter where you live. America’s trade deficit is averaging $500 B/year. Free trade is part of the cause of poverty, as well as family breakdowns. Free trade mostly destroys jobs. We are looking in a decline of quality rather than quantity of jobs. De-industrialization is occurring. Many major American companies are not American any longer; they are owned by foreign corporations. Boeing is losing manufacture of airplane wings to Mitsubishi. There is not a single airplane that doesn’t rely on parts from other countries.”

He stated, “Free trade simplified means there must be something good for both parties. Free trade is only one sided by the United States because many countries practice mercantilism. Trade is being manipulated to benefit our trading partners. The Euro currency has been manipulated to reduce the value of the currency of Germany to be lower by balancing it out with the economies of France, Italy, Spain, and Greece. The U.S. is being forced to compete with the state capitalism of Europe and Asia.”

He added, “Free traders say that trade deficit doesn’t a matter, but trade deficits mean that we consume more than we produce. David Ricardo’s theory of comparative advantage did not work when it was created and doesn’t work now. A nation needs some protection. Protectionism is really the American way. Alexander Hamilton was the founder of American protectionism. The U.S. had a protectionist policy until after WWII. Every country has done protectionism to succeed. He showed a chart showing the history of tariffs in the U. S.

He concluded, “After WWII, free trade became a policy because of the politics to win the Cold War. It is crumbling now because of politics. There are dangers in protectionism, but there are dangers in doing nothing. Treaties or trade agreements are basically about protecting property rights. The World Trade Organization has failed to enforce terms of current trade agreements and will not do any better with the proposed Trans Pacific Partnership Agreement.”

After the morning break, I provided a brief overview of California manufacturing prior to moderating our panel of manufacturers. California is the 8th largest economy in the world, and if it were a country, it would be equal to France. California lost 33.3% of manufacturing jobs between 2000 and 2009 compared to 29.8% nationwide, and lost 25% of its manufacturing firms.

I pointed out that even with its unfavorable overall business climate, California still ranks first in manufacturing for both jobs and output. However, since the Great Recession, California lags in manufacturing job growth at a 3.6% rate compared to the national 7.2% rate and a GDP growth rate in manufacturing of 11.2% in California compared to a 22.6% GDP growth in the U. S. as a whole.

On the positive side, California leads the nation in R&D and number of patents issued, and

California companies received $78.4 billion of VC dollars in 2015 (57% of U.S. total – up from 51% in 2010).

Mexico, Canada, China, and Japan are the top four export markets for California, and California represents 11% of total U. S. exports. California ranks second behind Texas in all exports, but

California ranks first among all 50 states in agricultural exports estimated at $13.6 billion per year. California is the biggest U. S. producer of nuts, dairy, ice cream, and wine. The top high tech export is computers and electronic products, which equals 26.1 % of all the state’s exports. Transportation goods are the second top export, consisting of airplanes, ships, unmanned vehicles, and underwater vehicles.

Besides the good weather, Southern California’s advantages are:

• Gateway to Pacific – two major ports – Long Beach and San Diego

• Major hub in western U.S. for air, rail roads & waterway transportation

• Skilled, educated workforce for ALL occupations

• Research Institutions and Universities

• Large inventor/entrepreneur pool

• Hundreds of business Incubators and Accelerators

• Angel investor networks

• Venture capital networks

• 18 Foreign Trade Zones

• Employment Training Panel funds for employee training

• Workforce Investment Boards

There is also an abundance of business resources in Southern California, such as the California Manufacturing Technology Consulting (designated California MEP), two Centers for Applied Competitive Technologies, several Small Business Development Centers and Economic Development Agencies, as well as many Chambers of Commerce and Business Councils.

I concluded with mentioning the opportunities we have to improve the California business climate, change our national tax and trade policies, return manufacturing to U.S. through reshoring, connect regional manufacturers with other U. S. suppliers, increase collaboration between manufacturers and community college to address workforce and skills gaps, and educate community/youth about career opportunities in manufacturing.

After my presentation, the following three panelists shared their stories:

James Hedgecock, Founder and President of Bounce Composites, which designs, engineers, and manufactures high-quality, durable composite goods for multiple industries, including wind energy, automotive, aerospace, and sporting goods. He shared that the company started out producing their own patented design of stand up paddleboards, but it has been tough to compete with offshore companies because of unfair trade practice. He said it was especially difficult to export to Mexico and Europe because Value Added Taxes (VATs) are added to the price of their products, making their product more expensive.

Robert Lane and Dave Mock, principals of Lane OPX, shared how they help companies optimize excellence through blending Lean Six Sigma principles, strategic business initiatives and participative management philosophies to grow organizations, and inspire high performing, motivated teams. By leveraging their deep experience in manufactur9ing, team dynamics, leadership development and organizational design, they have been able to power the turnaround of small to large companies. More recently, they have been able to help manufacturers return manufacturing to America from overseas.

Mr. Wei-Yung Lee, CEO of Carlsbad Technology Inc. was our final panelist. Based in Carlsbad, California, Mr. Lee said that Carlsbad Tech was founded 1990 and is a subsidiary of Taiwan’s leading YungShin Pharmaceutical Co. The company began as a contract manufacturer of generic pharmaceuticals and has become an industry leader in manufacturing and distribution of generics, supplements, and medical devices. He said, “We have 150 employees and 15 are well-trained chemists. We have the capacity to produce 60 million capsules and 400 million tablets per year. Last year, we Launched our Comfort Vision™ contact lenses in the USA and have sold over 1 billion units in Asia. We are striving to become a global health bridge, bringing a world of innovative health products to the markets that need them. ”

After the panel, Jill Berg, President of Advanced Test Equipment Rentals, told about the products and services of her company. They rent, lease, and sell a large selection of test and measurement equipment and other types of lab equipment to companies all over the world. She announced that her company was hosting a San Diego Test Equipment Showcase on October 18th.

Then, Chris Marocchi, Field Operations Manager of California Manufacturing Technology Consulting (CMTC), explained that his organization is a non-profit consulting organization that just won the competition to provide Manufacturing Extension Program services for all of California. These services provide innovation and growth strategies along with operational enhancements to foster profitable growth for California companies. MEP services include: innovate new products, open new markets, improve workforce skills, increase product quality and reduce costs through Lean training, increase energy efficiency and green production, and optimize supply chain performance.

After our lunch break, I presented information on Lean Six Sigma Institute (LSSI) as neither of the principals was able to attend and I had obtained my Yellow Belt Certificate in Lean Six Sigma from LSSI in 2014. LSSI is boutique-style training and consulting company that uses training and coaching model to guide companies to manage Lean Six Sigma change, develop internal leaders, and sustain the results. LSSI’s is headquartered in Chula Vista California, but has satellite offices located in nine countries and employs over 60 expert consultants worldwide. Lean and six sigma principles and tools apply to virtually any process, and LSSI has successfully helped clients implement Lean Six Sigma in a variety of industries, such as manufacturing, retail, and healthcare.

Our key note speaker for the summit was Michael Stumo, CEO of the Coalition for a Prosperous America, speaking on “Growing SoCal Manufacturing.” Mr. Stumo stated, “CPA is a true coalition

of manufacturing, agriculture, labor, Republicans, Democrats, Progressives, Conservatives, and Independents. Our members are: Trade Associations, companies, farm organizations, Labor Unions, and individuals from all walks of life. Our non-Agriculture industries are: manufacturers, steel, tooling and machining, electronics, textiles, copper, aluminum, etc. Our mission is to balance trade and produce more in America to reclaim American prosperity.”

Mr. Stumo explained that there is a difference between service jobs and manufacturing jobs. According to Investopedia, “Examples of service sector jobs include housekeeping, psychotherapy, tax preparation, legal services, guided tours, nursing and teaching. There are very few “tradable” service jobs. By contrast, individuals employed in the industrial/manufacturing sector might produce goods such as cars, clothing and toys.”

He said, “There is also a difference in income and purchasing power between manufacturing and service jobs. When considering what industry sectors to prioritize for workforce and economic development efforts, it is important to look beyond basic employment numbers. This is because, while a sector might have a lot of jobs, it might not actually be producing a lot of income for the region, which is also very important for overall economic health and vitality.”

Mr. Stumo stated, “The problem is that as more manufacturing jobs leave, more productivity leaves as well. Unlike manufacturing, service-sector jobs have strict limits in terms of productivity. For example, a live performance of Beethoven’s 5th requires the same amount of performers/employees as when it was performed early in the 19th century. Compare that with the production of almost anything manufactured — the number of workers now required to produce a bolt of fabric, for example.”

He added, “There is a regional ripple effect of service vs. manufacturing jobs. At $4.4 trillion in total sales, manufacturing is by far the biggest income generator in our nation, despite a fairly rapid decline in employment. Yet, manufacturing still manages to far outperform all other industries in terms of pure income creation. Manufacturing generates more income per worker and has much bigger ripple effects, creating much more impact in a region while helping to raise wages in lower-productivity service sectors.”

He asked the rhetorical question, “What’s wrong with a service economy? He answered, “It shrinks manufacturing employment as well as the manufacturing sector’s ability to prop up wages. A labor market that loses wage pressures of high-productivity manufacturing industries will settle at wage rates lower than markets where this wage-boosting effect is present. Economic development policy makers should be careful about shunning manufacturing or other production sectors in favor of service sectors. This is a problem because 66% of U. S. workforce is without a four-year college degree.”

He concluded stating, “America is at a crossroads. We are losing an economic competition against other nations whose mercantilist strategies are destroying our manufacturing jobs, critical industries, and our standard of living, our national security, the security of our food supply, and our children’s futures. For the U. S. to become prosperous again, our future strategy must include the following:

• National Priority of Balanced Trade

• Strong enforcement

• Stop new trade agreements to force a re-think.

• Neutralize currency manipulation

• Tax reform with VAT/consumption taxes

• Consider tariffs to neutralize imbalances

We have a choice. We can continue our current trade and tax policies or we can develop and implement a comprehensive strategy that retains and reinforces our leadership in innovation, locates investment and production in the U. S. and raises employment by creating good paying jobs.”

As chair of the California chapter of CPA, I hope you will join our efforts to make America prosperous again.