For the past three decades, outsourcing was the cornerstone of U.S. manufacturing. First, manufacturers outsourced to Mexico, Puerto Rico, and the Philippines. Then, manufacturers started outsourcing to China after it was granted Most Favored Nation status in the year 2000. As I have written in my three books and over 300 articles, returning manufacturing to America is critical to rebuilding America’s industrial base. This process became known as “reshoring” after Harry Moser founded The Reshoring Initiative in early 2010. Returning manufacturing to America through reshoring is critical to rebuild America’s industrial base to ensure that we have the commercial and military/defense products needed to keep Americans healthy and safe

I had the honor of being an early supporter/collaborator of The Reshoring Initiative after I wrote about why it was important to understand “Total Cost of Ownership” when selecting vendors to manufacture products. I based my opinion on the hard copy worksheets of the National Tooling & Machining Association and the American Mold Builders Association. Harry Moser called me after reading my article and told that he had just founded The Reshoring Initiative and “created the Total Cost of Ownership Estimator® – a free online tool that helps companies account for all relevant factors — overhead, balance sheet, risks, corporate strategy and other external and internal business considerations — to determine the true total cost of ownership.” He trained me in how to give presentations on TCO and authorized me to be a substitute speaker for him on the West Coast or when he had a scheduling conflict for a trade show or conference. Every year, Harry provides me with new data so that my presentations remain consistent with his presentations.

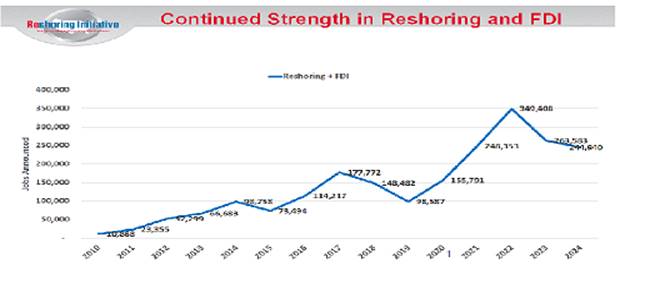

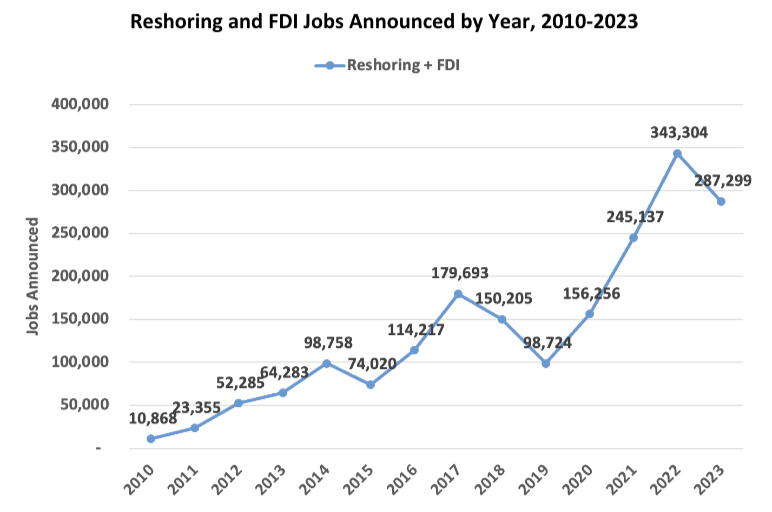

The good news is that reshoring is rapidly increasing and making a significant impact on U.S. manufacturing, driven by supply chain resilience, geopolitical risks, and government incentives. According to the 2024 Reshoring report by The Reshoring Initiative, “244,000 jobs were announced in 2024; 1.7 million jobs have been filled since 2010.” Reshoring is improving our country’s self-sufficiency capacity for goods essential to our economy and national security according to a number of surveys and reports that I highlighted in my article titled, “Is Reshoring Making a Difference and Increasing?” published March 19, 2025.

When I asked Harry why he started the Reshoring Awards, he responded, “We started the Awards, initially as a feature of the NTMA/PMA Purchasing Fairs that connected industrial buyers with contract manufacture providers of machined components and tooling. When the Fairs ended, we promoted the awards to the national industry and included AMT, SME and FMA as supporters.” He added, “We wanted to establish a Reshoring Award to “motivate more companies to reevaluate their offshoring and see that it is often more profitable to produce or source domestically. We hoped that other associations would choose to support similar awards to show that their industries are now successfully reshoring.”

On May 25, 2017, The Reshoring Initiative andPrecision Metalforming Association (PMA)invited companiesthat have “successfully reshored parts or tooling made primarily by metal forming, fabricating or machining to apply forthe First National Reshoring Award. There was one award for buyers and one award for suppliers.” To be eligible for an award, a product or component has to meet the following criteria:

- Reshoring or foreign direct investment (FDI) of the work occurred between Jan. 1, 2010, and the year prior to the year’s award. April 30, 2026.

- Work had to be returned to North America from outside North America.

- The products, parts, or tooling reshored must be made primarily by forming, casting, fabricating, or machining, including additive machining.

The criteria for winning are:

- Number of North American jobs created

- Dollars per year of sales reshored or nearshored from further offshore

- Capital investment

- Product innovation

- Process innovation

- Success of the project

- Completeness of application

Bonus points are awarded to PMA, AMT, SME, FMA, and NTMA members. Winners include companies ranging from 20 to 15,000+ employees.

On October 31, 2018, AMT (The Association For Manufacturing Technology) and NTMA (National Tooling and Machining Association) joined the Reshoring Initiative and Precision Metalforming Association (PMA) to invite “Companies that have successfully reshored products, parts or tooling made primarily by metal forming, fabricating, casting or machining, including additive manufacturing,” to apply for the award…the work must have been reshored between January 1, 2013, and December 31, 2018, from outside North America to North America.”

These four organizations have continued to grant Reshoring Awards every year since 2018. The winners by year are:

2018 – Mitchell Metal Products, located in Merrill, WI

2019 – Sherrill Manufacturing, located in Sherrill, NY

2020 – Die-Tech & Engineering, located in Walker MI

2020 – Trenton Forging, located in Trenton, MI

2021 – ACME Alliance, located in Tempe. AZ

2022 – Hardinge, located in Elmira, NY

2023 – Hobson & Motzer, located in Durham, CT

2024 – Sumitomo Drive Tech., located in Chesapeake, VA

2025 – Marlin Steel, located in Baltimore, MD

2025 – GE Appliances, located in Louisville, KY

The 2026 Award will be presented at IMTS 2026 to be held September 14-19, 2026 at McCormick Place, Chicago, IL. The event will take place on the Main Stage between the North and South Halls, probably at 9am on Sept 17th. Applications are due by May 31, 2026. The application form is located at https://www.amtonline.org/article/reshoring-award. You may email Harry Moser at <harry.moser@reshorenow.org> for a file for applying.

While each of the above recipient companies may have had a variety of different reasons for reshoring using the Total Cost of Ownership Estimator®, the reality is that companies will only bring back the majority of offshored work if the economics of producing in the U.S. justifies doing so.

In last year’s Reshoring Report cited above, The Reshoring Initiative issued a call for smarter industrial policy that included the following to increase reshoring:

- Massive investment in skilled workforce development (modeled after German apprenticeships).

- A 20% lower USD to improve global cost competitiveness.

- Retention of immediate expensing of capital investments.

I agree with these recommendations and have expressed in previous articles that the actions needed to achieve more reshoring are the same as needed for rebuilding manufacturing in general. These include developing a national manufacturing strategy that encompasses corporate tax reform, regulatory reform, Border Adjustable Taxes (aka VATs), and a Market Access Charge while addressing the predatory mercantilist practices of other countries with regard to currency manipulation, product dumping, and government subsidies.

President Trump has addressed tax reform and regulatory reform, but the other recommendations still need to be addressed. While we can take advantage of tariffs being a key motivator for reshoring now, we need to have other beneficial policies in place for the future to have long-term growth of our domestic manufacturing base.