To learn more about why there is such a concentration of musical instrument manufacturers in Northeast Indiana, I interviewed John Stoner, president and CEO of Conn-Selmer, Inc., a subsidiary of Steinway Musical Instruments, Inc. I learned that the history of making musical instruments really started with this one company. Today, Conn-Selmer has a portfolio of musical brands that has made it the leading manufacturer and distributor of band and orchestra musical instruments and accessories for student, amateur and professional use.

I asked Stoner about the origins of the Selmer Company, and learned that the main Selmer Company is still located in Paris, France. The history of the U.S. company dates back to the early 1900s. It has production facilities in Elkhart, Ind., Eastlake, Ohio and Monroe, N.C.

Next, I asked where the Conn part of the name of the company came from, and Stoner said, “C. G. Conn started a company in Troy, Mich., and then he moved to Elkhart, Ind. The company manufactured brasswinds, saxophones and electric organs in the 1950s.”

When the Selmer company acquired CG Conn, the brands Armstrong and King were part of the acquisition. Later, they acquired the LeBlanc Corporation, which brought another family of brand names such as Leblanc, Vito, Holton, Martin, and the distribution rights to Yanagisawa – making Conn-Selmer the largest U.S. full-line manufacturer of band and orchestra instruments.

“We have a strong portfolio of instruments made here in Elkhart. Seventy percent of our products are manufactured here in the United States and sold globally. The other 30 percent are manufactured in France, Japan and other parts of the Asia Pacific and sold in various parts of the world.” Stoner said.

When I asked if the company had implemented Lean principles and tools, he said, “I looked at Lean when working in a previous industry, and I brought the concepts over to Conn-Selmer. We applied Lean principles so that we could be in a position to be more competitive when there was an upturn after the 2009 recession.”

He added, “Northeast Indiana is a hot bed for musical instruments. At one time there were about a hundred manufacturers of instruments. Over the years, people would leave a company and start their own company to make a musical instrument. Elkhart became the musical instrument center of the country.”

In my interview with Tony Starkey, president of Fox Products, I learned about the interesting history of another musical instrument company.

Starkey said, “I was an owner of a machine shop before I came to Fox Products. Fox Products is located in South Whitley, a small community of less than 2,000 people, about 10 miles from Fort Wayne. I used to mow the lawn for the company when I was 13. The company was founded by Hugo Fox in 1949 after he retired from being the Principal Bassoonist for the Chicago Symphony and returned to his hometown. He had the goal of making the first world-class bassoon in the U.S. He started the business in a modified chicken coup on the Fox family farm, and it took him two years to successfully make a bassoon.”

Later, Hugo’s son, Alan, left his career as a chemical engineer and ran the company for over 50 years, applying engineering principles to making instruments. Fox owned the student market because Alan made the instruments much easier to play.

The first Fox oboes came out in 1974. Later that year, a fire destroyed the woodshop and reed-making equipment, so Alan used other sites in South Whitley to keep the company alive while a new plant was being built. The company expanded and started making English Horns in 1999.

Since Starkey became owner in 2012, the company has grown 30 percent. It now has 130 employees.

“When I took over the company, we didn’t have any prints for the instruments. We had 3D models and patterns and tools in Germany. We had to start over and reverse engineer the instruments to create the drawings. Now, we are able to work in Solidworks and have CNC machines to make the metal parts. We even set up our own silver plating line,” Starkey said. “Indiana is a great business state and a great place to have a business. We did a turnkey operation for our silver line without a lot of regulations and delays.”

I asked if they have applied Lean principles and tools to the company. Starkey said, “I hired people who have a Lean background, so we are using technology and implementing Lean wherever we can, taking the human factor into consideration. We are hoping to get to be where we want to be as a Lean company in about two to three years.”

Last of all, I interviewed Bernie Stone, founder and president of Stone Custom Drum Company. Stone said, “I played drums in a marching band in high school. Then, I worked in a musical instrument store and started doing repair of drums and projects for the percussionists of the symphony.”

He explained, “In 2002, I had the opportunity to purchase the drum shell manufacturing equipment, tooling and assembly line from the Slingerland Drum Company, one of the legendary vintage American drum brands. It gave me the opportunity to own the shell-shaping molds and tools, so I invested my money – and my life – into bringing them up to 21st century standards and crafting Super Resonating® shells that surround punchy tom strokes with full, fat tone, make bass drums kick with big and round low-end responses, and snares cut with a crisp articulate ‘snap’ that sings with resonance. I bought some other equipment I needed on eBay and some from the Gretsch Company, another drum company. I learned how to operate the equipment and reverse engineered the drums.”

He added, “I started my own company as a LLC in 2011. I am now looking to expand into a S corporation to get investors to grow the company. I think the skill set we have as a company is unique as very few people know how to make a great drum set. We manufacture our own Stainless Steel and brass tune lock fixtures to keep the drum in tune.”

I asked what kind of drums he makes – drums for rock and roll bands as well as for the symphony. Fort Wayne has a great philharmonic, which is a stepping stone to bigger and more prestigious symphonies. For example, Pedro Fernandez started at Fort Wayne and then went on to San Diego and is now at the Houston Symphony.

“The reason I am in Fort Wayne to make drums is that all the suppliers I need are within 50 to 100 miles for the wood, metals, tool and die shops, 3D printing, etc.,” Stone said.

From these stories, we can see that the musical instrument industry had developed gradually over the last hundred years or so from one company spinning off from another company or one company acquiring another or buying the rights to a brand name.

The craftmanship legacy of the Northeast Indiana region’s workers has played a big role in the success of many companies, along with a strong supply chain of subcontractors and materials. It is likely that the region will keep fostering the development and growth of new musical instrument companies to support the strong creative musical arts community of Northeast Indiana.

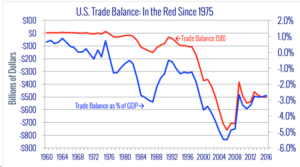

Source: Coalition for a Prosperous America

Source: Coalition for a Prosperous America